Getting the UK back to work and how the new CJRS is operating.

On 1st June the Government announced the latest support scheme for supporting the UK’s employers as outlined in our previous post 'CoronavirusJob Retention Scheme and SSP Update' . The Coronavirus Job Retention Scheme (CJRS) was designed to protect jobs by paying the wages of furloughed staff.

As the government focusses on restarting the economy and getting people back to work, easing of lockdown restrictions and are allowing many more businesses to open from 4 July. To support this the CJRS is changing to allow a flexible furlough option and a phased reductions in claims.

On Saturday 14th June the long awaited detail behind the scheme was finally released.

This phase two of the Coronavirus Job Retention Scheme is excellent news for employers as it allows previously furloughed employees to enter into a new flexible furlough arrangement and return to work on a partial basis. This new phase comes into effect from 1st July.

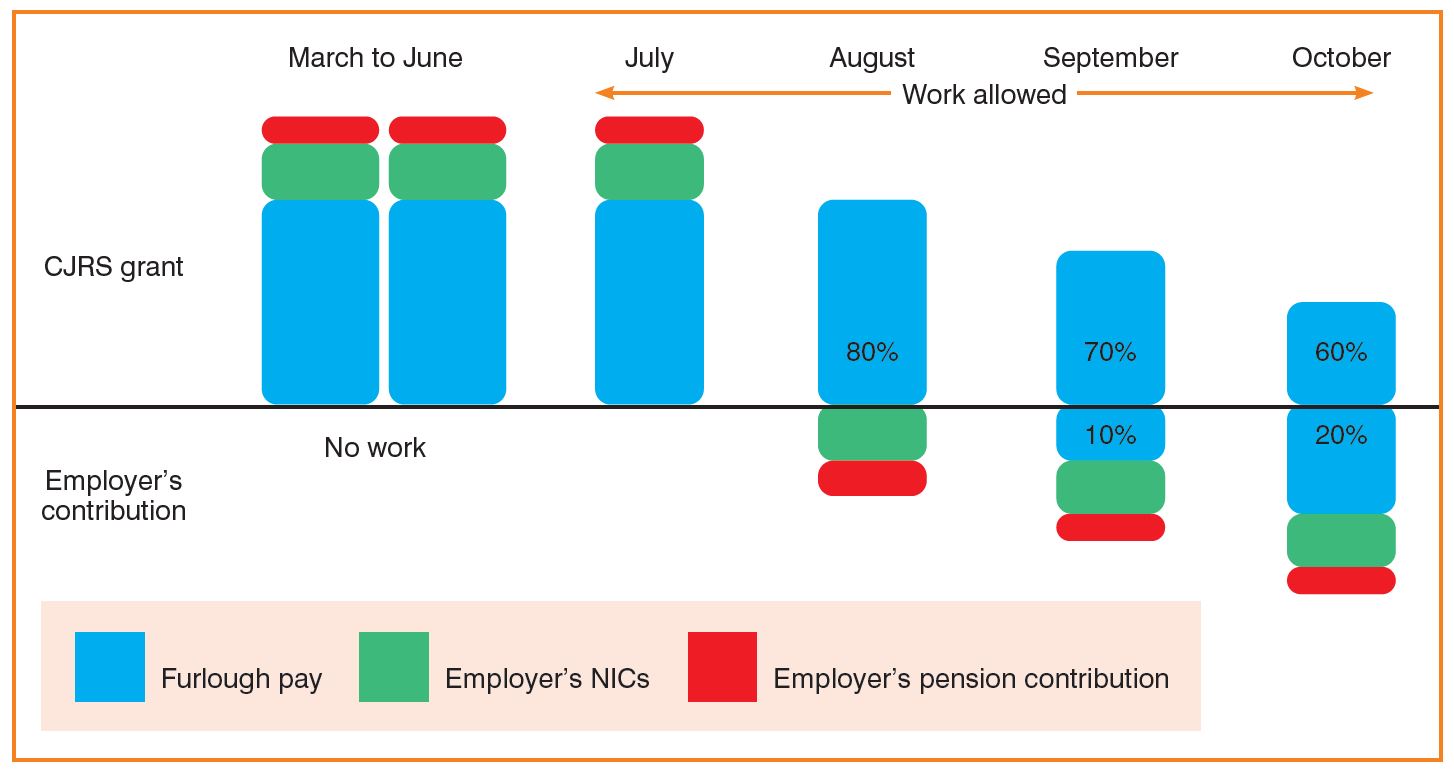

As employer you pay for the work undertaken at their full rate and the Government picks up the remainder at the support rates that are also varying as the scheme winds to a close on 31st October 2020.

This new flexibility sees a shift in the basis of calculating furlough payments and claims from a daily rate to an hourly one. Coupled with the reducing amount of support from the Government, or more accurately, the increasing size of the employer contribution the computations and claims are now becoming very complex.

Summary of key changes

ELIGIBILITY

- No new staff can be furloughed onto the new scheme, only those who have already been furloughed by 10th June (maternity & paternity exemptions apply).

- Only staff who have been previously furloughed for a minimum of 21 days can be included.

- A new formal agreement is needed, although the employee does not need to sign it.

- There is no 3 week minimum period for the flexible furlough, up until the scheme ends on 31st October.

- Employees are allowed to work part time hours unlike with the previous scheme where the HMRC were being very strict about no work being done.

CLAIMS

- The minimum claim period is 7 days although this can be shorter for the first and last days in a month. So if an employee works 2 days in a 7 day period, the claim would cover that 7 day period on the HMRC portal.

- There is a maximum claim period of 1 calendar month, so claims cannot be aggregated across months i.e. July and August, and made into one claim.

- New requirements for accurate hours work mean you can only claim 14 days in advance but cannot claim for July before the 1st July. Because of the need for accurate hours worked, it may be worth waiting to claim towards the end of the month so you can be sure employees have actually worked these hours, rather than basing a claim on an assumption that they will work those hours.

- Claims must now be calculated based on the balance between ‘usual’ hours worked minus the actual ‘worked’ hours.

Calculating Claims

The main change is that the computations for claims now move from full calendar days to an hours worked basis. This allows employees to return to work on a part time basis, with the CJRS scheme topping up their wages if required.

The complexity comes in when calculating ‘usual’ pay and ‘usual’ hours, especially when looking at non-salaried employees

Salaried employees

The usual pay per day is calculated by identifying an employee’s earnings in the last pay period filed with HMRC before 19 March.

Divide by the days in that period

Multiple by 80%

This gives your usual pay per day (but it is capped at £80.65 for July)

The usual hours per day is calculated by identifying the contracted hours in the last pay period before 19 March.

Divide by the number of calendar days in the period

Variable paid employees

To calculate usual pay per day, use the higher of either the average wages for the tax year 2019/2020 or the corresponding calendar month in 2019/20 i.e. July 2019

Multiply by 80%

This gives your usual pay per day (but it is capped at £80.65 for July)

Usual hours per day are calculated by taking the higher of the daily hours for either the average hours worked per day for the tax year 2019/2020 or the average hours worked per day in the corresponding period last year.

Once the claim period is decided,

- Usual hours per day x number of days in claim period = usual hours in a claim period (round up to nearest whole number)

- The difference between usual hours worked and actual hours worked = furlough hours in claim period

- Usual pay divided by usual hours in claim period = hourly rate for furlough hours

Changes to the amounts recoverable

From August, the amount you can recover from HMRC for furlough amounts paid to employees is reducing.

August

You will no longer be able to recover Employers NI or Employers Pension Contributions.

September

80% furlough value must be paid to employees but employers are expected to contribute 10%.

October

80% furlough value must be paid to employees but employers are expected to contribute 20%.

Key Takeaways

- The new scheme gives greater flexibility for employers to partially return their employees to work

- New flexible furlough contracts are needed with employees. These must be confirmed in writing and retained for 5 years

- Claims need to effect actual hours worked, so this may result in the timing of claims needing to be delayed for accuracy

These changes, although good for businesses, will put an added strain on payroll teams as they battle to make sense of this complexity and changes. At Dataplan we continue in our commitment to our clients to work through these computations and submit claims on their behalf at no additional charge.

Dataplan are one of the UK’s leading providers of specialist payroll and associated services.

From payroll outsourcing and pension service management to ePayslips and gender pay gap reporting; we have a solution for you and your business.